USA Facility Management in Education Hits USD 48B on Smart Tech Push | Ken Research

The biggest inefficiency in American education is not in classrooms. It is in the buildings around them: aging HVAC systems, deferred maintenance backlogs, and facility management contracts that have not been renegotiated since before energy efficiency mandates existed. As per Ken Research market modelling, the USA facility management in education market is valued at USD 48 billion in 2024, with 65% of institutions now implementing green sustainability initiatives and smart technology integration projected to reduce operational costs by up to 30%. The full competitive landscape and segment forecasts are available in the USA Facility Management in Education Market Report.

This analysis draws on data from Ken Research market modelling, U.S. Department of Education funding disclosures, APPA educational facilities data, and independent FM sector benchmarking.

USD 48 Billion in 2024: How K-12 Public Schools Drive the Market While Higher Ed Scales Smart Technology

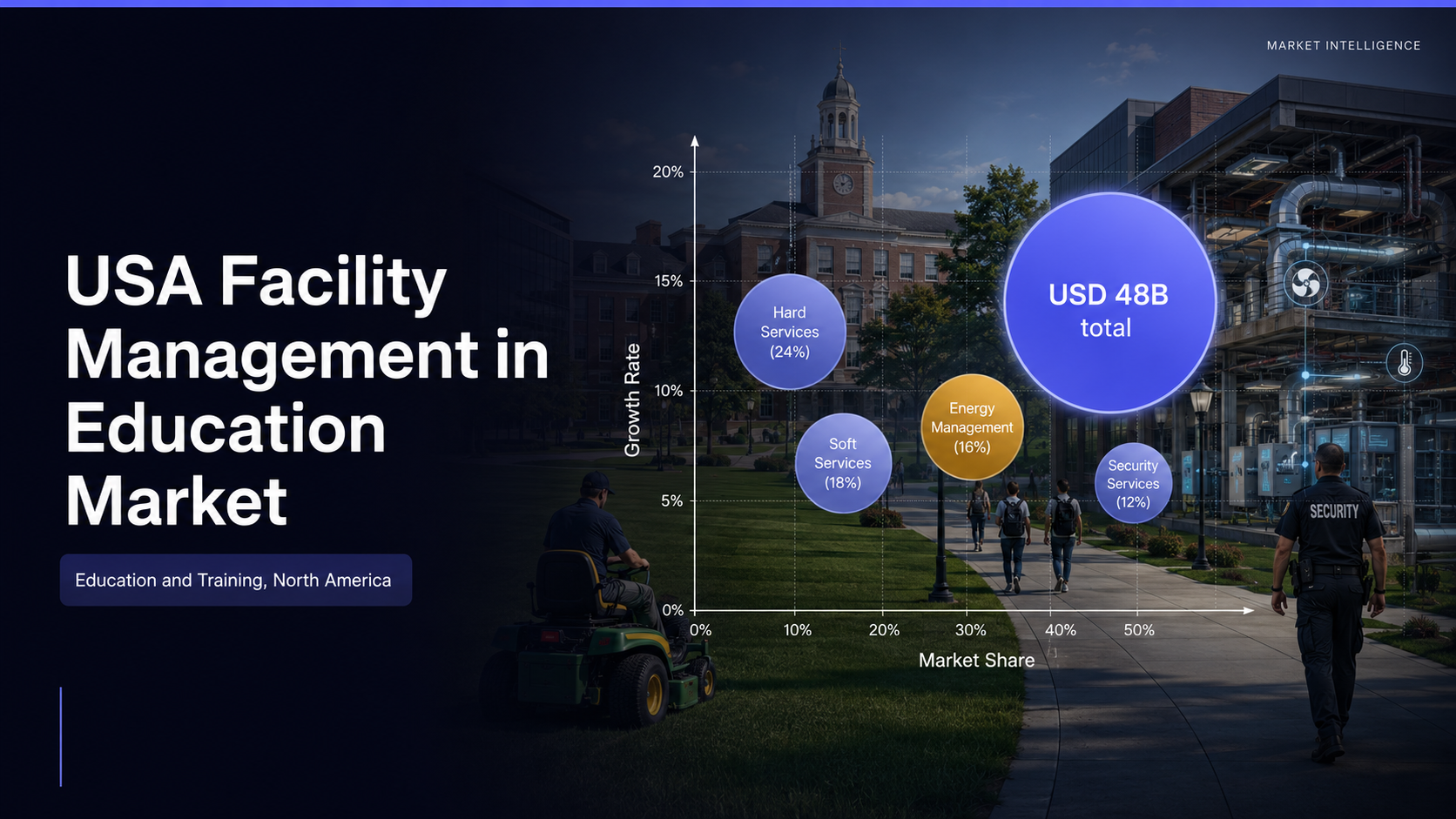

The USA education facility management market is valued at USD 48 billion in 2024, with K-12 public schools representing the largest single end-user segment. The market spans hard services (HVAC, electrical, plumbing), soft services (cleaning, landscaping, security), and integrated facility management contracts. Aramark leads K-12 outsourced contracts, while CBRE and JLL dominate higher education integrated FM. Facility management software alone is projected at USD 1.5 billion by 2025, as BIM and AI adoption accelerates across university campuses. For operators benchmarking adjacent institutional FM markets, the USA Facility Management in Data Centers Market reveals how the same smart technology stack is delivering superior cost reduction in mission-critical environments.

- K-12 Public Schools: Largest segment, with Aramark and Sodexo leading outsourced contracts across New York, Los Angeles, and Chicago metro districts.

- Higher Education: CBRE, JLL, and EMCOR Group lead integrated FM contracts, with smart technology adoption driven by energy efficiency mandates and deferred maintenance backlogs.

- Sustainability Push: 65% of institutions implementing green initiatives, with energy-efficient system upgrades generating potential annual savings of up to USD 2 million per campus.

ESSA Mandates and Smart Tech: How Regulatory Compliance Is Reshaping Outsourcing Decisions

The Every Student Succeeds Act (ESSA) compliance requirements, alongside ADA standards and environmental protection regulations, have elevated facility management from an operational cost center to a legal compliance imperative. Smart technology integration, including BIM, AI-powered predictive maintenance, and IoT building management systems, can reduce operational costs by up to 30%, making the upgrade case compelling for budget-constrained districts. The USA Facility Management and Smart Infrastructure Market maps how the same smart building technologies are reshaping operational cost structures across the broader institutional sector, providing direct benchmarks for education FM contract pricing.

- Regulatory Compliance: ESSA mandates, ADA standards, and energy efficiency regulations create non-discretionary FM spending across all K-12 public school districts.

- Smart Technology ROI: Operational cost reductions of up to 30% achievable through BIM, AI predictive maintenance, and IoT building management system integration.

Which FM providers are winning the largest K-12 and higher education contracts as the USD 48B market consolidates around smart tech capabilities? Download Sample Report to see competitive benchmarks and segment analysis.

Why Is 45% of the Education FM Market Constrained by Budget Shortfalls Despite Growing Demand?

Budget constraints affect 45% of institutions reporting funding shortfalls, while a 35% skilled workforce vacancy rate limits service delivery capacity. This paradox, high demand met by constrained supply, is creating a consolidation dynamic where large integrated FM providers with scale economies can underbid on labor and technology while smaller operators exit. Public-Private Partnerships (PPPs) are emerging as the primary mechanism for closing the gap, enabling institutions to upgrade to smart FM infrastructure without upfront capital commitments.

USA Education FM Outlook to 2030: Smart Building Mandates and Sustainability Drive the Next Phase

The USA education FM market is on a sustained growth trajectory through 2030, driven by smart building adoption, sustainability mandates, and rising online learning infrastructure needs. The U.S. Department of Education's infrastructure investment programs are creating capital deployment windows for FM providers. The broader USA Facility Management Market is projected to reach USD 442.89 billion by 2030 at a 5.8% CAGR, with education remaining one of the highest-concentration segments for outsourced contract growth.

- Market Scale: Education FM within a broader US FM market projected at USD 442.89 billion by 2030 at 5.8% CAGR.

- Online Learning Infrastructure: 35% increase in course offerings projected, requiring expanded digital infrastructure maintenance contracts alongside traditional hard services.

- Energy Efficiency: Smart system upgrades generating up to USD 2 million in annual savings per campus are accelerating outsourcing decisions as budget-constrained districts seek provider-financed upgrades.

What FM Providers, Institutions, and Investors Must Do Before Smart Building Mandates Lock In Incumbents

The USA education FM market is entering a technology-differentiation phase: providers with smart building capabilities will lock in long-term integrated contracts while traditional hard-service-only operators lose share. For a segment within a market valued at USD 48 billion in 2024, the first-mover advantage in smart FM contract design is compounding rapidly.

- FM Providers: Build BIM and IoT integration capabilities to compete for 65% of institutions targeting green sustainability mandates and the 30% cost reduction smart technology enables.

- Educational Institutions: Negotiate PPP structures that enable smart infrastructure upgrades without upfront capital, eliminating the 45% funding shortfall barrier to FM outsourcing.

- Investors: Target integrated FM platforms with smart building technology stacks: the 35% workforce vacancy rate rewards technology-substituted service delivery over labor-intensive models.

See the full competitive provider map and smart technology adoption forecast across K-12 and higher education. USA Facility Management in Education Market Report covers segment-level analysis and policy impact forecasts through 2030.

Conclusion

The USA education FM market has reached an inflection point where smart technology adoption separates the FM providers that will hold multi-year integrated contracts from those that will be displaced by consolidation. The USD 48 billion market base and the 30% cost reduction potential from smart building systems are making the business case for outsourcing unavoidable, even for the 45% of institutions reporting budget shortfalls. The strategic question is not whether to outsource: it is which technology-enabled provider earns the long-term contract. Access the USA Facility Management in Education Market Report for the full analysis.

Frequently Asked Questions

Q1: What is the size of the USA Facility Management in Education Market?

The USA Facility Management in Education Market is valued at USD 48 billion in 2024, with K-12 public schools as the dominant end-user segment. The broader US FM market is projected at USD 442.89 billion by 2030 at a 5.8% CAGR, with education among the highest-concentration sectors for outsourced contracts.

Q2: Who are the key players in the USA education facility management market?

Key players include Aramark, Sodexo, CBRE Group, JLL, ABM Industries, EMCOR Group, and Compass Group. Aramark specializes in K-12 outsourced FM, while CBRE and JLL dominate higher education integrated contracts. Facility management software is projected at USD 1.5 billion by 2025, with AI-driven platforms gaining market share from legacy providers.

Q3: What is driving growth in the USA Education Facility Management Market?

Three primary drivers: 65% of institutions implementing green sustainability mandates, smart technology ROI of up to 30% cost reduction, and ESSA regulatory compliance requirements creating non-discretionary outsourcing demand. Public-Private Partnerships are closing the funding gap for 45% of budget-constrained institutions.

Q4: How does ESSA affect the USA education FM market?

ESSA mandates create non-discretionary facility compliance spending across all K-12 districts, alongside ADA and EPA regulations. 45% of institutions report funding shortfalls despite compliance requirements, with smart technology upgrades generating USD 2 million in annual savings increasingly funded through PPP structures rather than district budgets.

Q5: What is the impact of smart technology on USA education facility management?

Smart technology integration reduces operational costs by up to 30% per campus through BIM, IoT building management, and AI predictive maintenance. Facility management software is projected at USD 1.5 billion by 2025. For retail and commercial FM smart technology benchmarks, see the USA Facility Management in Retail Chains Market.

For the full competitive benchmarking, segment-level forecasts, and policy impact analysis, access the USA Facility Management in Education Market Report from Ken Research, covering facility management across North America.

Comments

Post a Comment