Saudi Arabia Logistics Real Estate Market Outlook 2024-2030: Forecast

Saudi Arabia Logistics Real Estate Market Outlook 2024-2030: Forecast

Executive Summary

Saudi Arabia's logistics real estate market reached USD 13 billion in 2024. One ambition defines it: Vision 2030 aims to make the Kingdom a global logistics hub, so warehouses, cold storage, and logistics zones are being built at national scale.

Key Market Velocity Data

- Current Market Value: USD 13 billion in 2024

- Projected Market Value: approximately USD 22 billion by 2030

- CAGR: about 9% during 2025 to 2030

- Dominant Segment: warehousing and distribution centers, e-commerce-led

- Primary Growth Catalyst: Vision 2030, e-commerce growth, and logistics-hub investment

What Is Driving the Market?

Vision 2030 is the engine. The market sits at USD 13 billion in 2024 and is projected toward USD 22 billion by 2030 at about 9% CAGR. The government has allocated about SAR 100 billion, roughly USD 27 billion, to logistics infrastructure, with 18 purpose-built logistics zones planned. No other Gulf economy is investing in logistics property at this scale, and that state push underwrites the entire demand curve.

E-commerce and trade add pull. Online retail is projected toward SAR 50 billion, about USD 11.9 billion, growing roughly 30% a year, while Saudi ports handle over 10 million TEUs annually. Grade A warehousing and fulfillment centers are scaling to match. Foreign capital is flowing in as 100% ownership liberalization and special economic zones open the market.

- State funding: about SAR 100 billion (USD 27 billion) allocated under Vision 2030

- E-commerce: online retail heads toward SAR 50 billion, growing about 30% yearly

- Trade scale: Saudi ports handle over 10 million TEUs annually

- Zones: 18 purpose-built logistics zones anchor demand for modern facilities

Which Entities Are Shaping the Market?

Developers and REITs anchor supply. JLL Saudi Arabia, SISCO, Al Rajhi REIT, Agility Logistics Parks, and LogiPoint develop and manage warehousing and logistics parks across the USD 13 billion market, where warehousing dominates by type. Operators like DHL Supply Chain, Aramex, GAC, and Bahri occupy and run space. Scale, location near ports, and Grade A specification define the leaders, and REIT-backed development is accelerating institutional investment.

3PL and e-commerce tenants drive absorption. Retail and e-commerce tenants take the largest share of modern space, while pharmaceuticals and food and beverage drive cold-storage demand across the USD 13 billion market. Distribution and fulfillment centers lead by type, and the retail segment is the largest end-user. Build-to-suit and multi-client warehouses are absorbing the bulk of new demand.

Policy enables the build-out. New land-use rules, tax incentives in special economic zones, and 100% foreign-ownership liberalization shape investment, while environmental standards govern construction. These reforms pull global capital into the USD 13 billion market. Free-zone incentives now make Saudi logistics property globally competitive.

How Do Assets and Tenants Split?

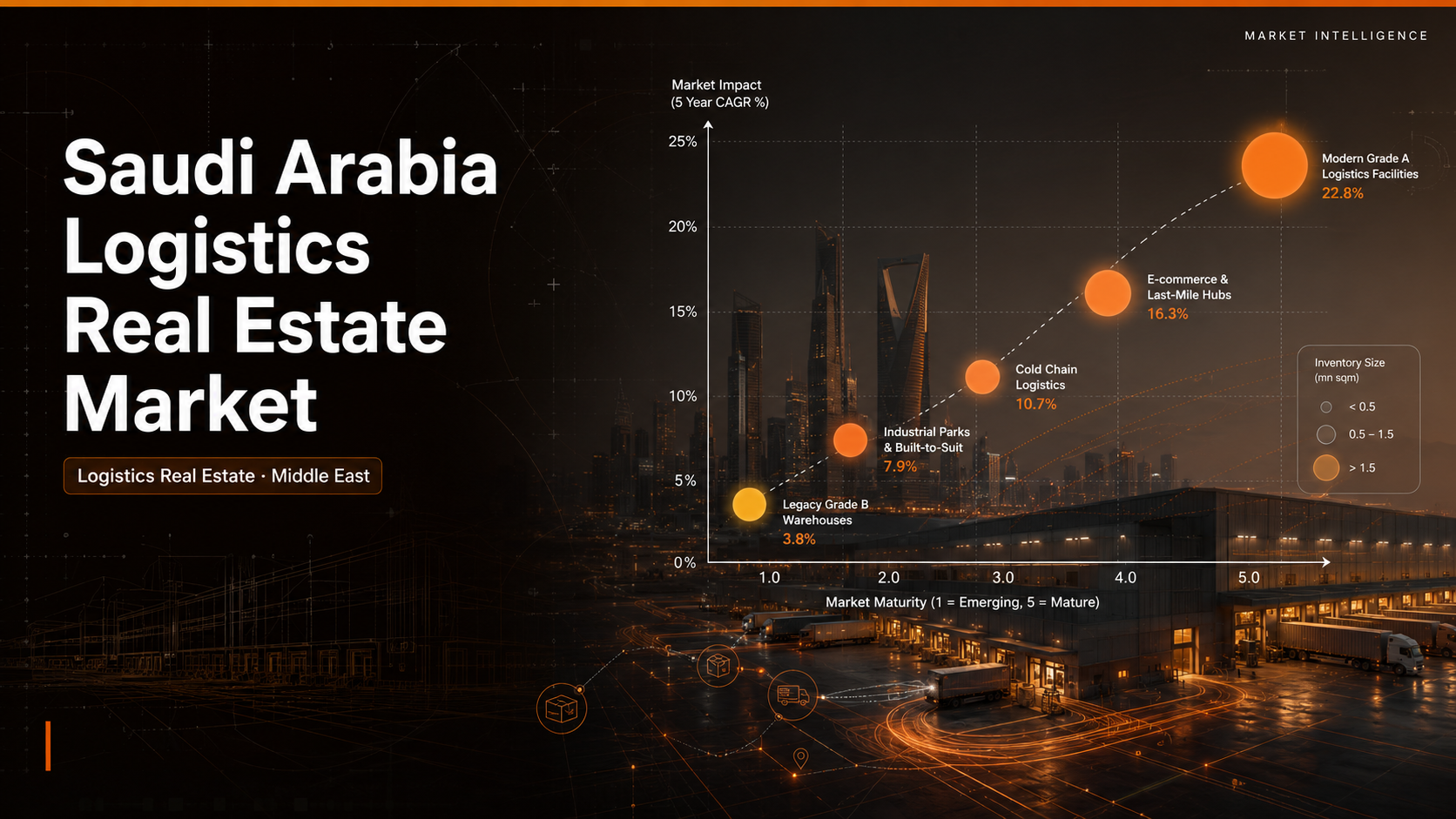

Assets and tenants concentrate demand. Warehousing, distribution centers, and fulfillment lead, ahead of cold storage and cross-docking. Retail and e-commerce dominate end-use across the USD 13 billion market in 2024, followed by manufacturing and pharmaceuticals. Cold storage and last-mile hubs are the fastest-rising. Cold storage is projected near SAR 5 billion, and smart logistics investment near SAR 3 billion. Grade A and SEZ-located assets command premium rents.

- By type: warehousing and distribution centers lead, with cold storage rising fastest

- By tenant: retail and e-commerce dominate, with pharma and F&B next

- By location: industrial zones, SEZs, and port-proximity sites command demand

- By spec: Grade A and smart-enabled facilities capture premium rents

What Does This Mean for B2B Decision-Makers?

Build Grade A near ports and zones. The USD 13 billion market grows about 9%, but the durable edge is modern, well-located, SEZ-eligible facilities serving e-commerce and trade. Developers with cold-storage and smart-warehouse capability will win. Vision 2030 zone alignment is the single biggest siting decision for new assets.

Specification and location are the levers. Grade A space, cold-chain capability, and SEZ incentives separate scaled developers across a USD 13 billion market heading toward USD 22 billion. Construction cost and timing are the real execution risks, and REIT structures unlock institutional capital for expansion.

- For developers: build Grade A, cold-storage-ready facilities in SEZs and near major ports

- For investors: back logistics REITs riding a 9% CAGR toward USD 22 billion

- For 3PLs: secure modern space early to serve e-commerce growing about 30% a year

- For occupiers: use SEZ incentives and 100% ownership to anchor regional distribution

Ken Research Strategic Outlook

Ken Research sees Saudi logistics real estate as a Vision 2030-driven build-out story. The next phase rewards developers and investors delivering Grade A, cold-storage, and SEZ-located assets that serve e-commerce and the Kingdom's logistics-hub ambition. Expect the USD 13 billion market to grow toward USD 22 billion by 2030 as government investment, foreign capital, and online retail compound across the Kingdom.

Data Source and Full Analysis

For deeper segment-level analysis, access the full Ken Research report here: Saudi Arabia Logistics Real Estate Market Report

Comments

Post a Comment