India Wine Market Outlook 2024-2030: Growth, Domestic Players, and Import Trends

India Wine Market Outlook 2024-2030: Growth, Domestic Players, and Import Trends

Executive Summary

India's wine market is moving from a metro novelty into a premium beverage category. A widening urban millennial base, rising wine tourism, and aggressive domestic capacity expansion are pushing the market toward USD 1,016 Million by 2030, reshaping how producers and importers compete for shelf and on-trade space.

Key Market Velocity Data

- Current Market Value: USD 574 Million in 2024

- Projected Market Value: USD 1,016 Million by 2030

- CAGR: 10% during 2024 to 2030

- Dominant Production Hub: Maharashtra with over 85% of output, led by Nashik

- Primary Growth Catalyst: urban millennial demand and wine tourism

What Is Driving Demand in the India Wine Market?

Demand is broadening on three fronts. India counted more than 5 million wine consumers in 2023, concentrated in metro centers, while Nashik wineries drew over 250,000 tourism visitors the same year. Still wine holds the dominant product share and red wine leads by color, as premium hospitality adoption pushed past 1.5 million bottles in 2023.

- Demand shift: a base of 5 million-plus urban consumers widens beyond occasional drinkers as premiumization takes hold.

- Tourism pull: 250,000-plus annual visitors to Nashik convert estate experiences into repeat at-home purchases.

- Channel change: off-trade now leads distribution, with e-commerce and modern retail expanding reach beyond hotels and bars.

- Import pressure: imported wine holds roughly 33% of the market, led by Spain, France, Australia, Italy, and Chile.

How Do State Policy and Regional Supply Shape the Market?

State policy is the decisive lever. Maharashtra's Grape Processing Industrial Policy 2022 disbursed INR 40 crore in 2023 and supported a 30% rise in production capacity, while Karnataka runs the country's only Karnataka Wine Board and offers a grape subsidy of INR 50,000 per hectare for new plantations (Karnataka Wine Board).

Production is geographically concentrated. Maharashtra accounts for more than 85% of output, centered on Nashik and Sangli, Karnataka adds about 10%, and other states make up the remaining 5%. High state excise duties remain the main brake, taxing wine alongside hard spirits and inflating shelf prices against global benchmarks.

Which Companies Are Shaping the Competitive Landscape?

The domestic field is highly consolidated. Sula Vineyards leads with close to 60% of the domestic market and reported INR 600 crore in revenue in FY25, far ahead of Fratelli Wines at 25% to 30% share and INR 276 crore, while Grover Zampa holds near 7% with INR 64.4 crore.

Capital is flowing to the challengers. In October 2024, AV Thomas Group infused USD 10.4 Million into Grover Zampa for new vineyards, tourism upgrades, and machinery. York Winery and Charosa Wineries round out the Nashik premium tier, leaving little room for sub-scale entrants without estate land or distribution reach. The arrival of foreign capital signals growing confidence in the long-run trajectory of the category.

What Does This Mean for B2B Decision-Makers?

For producers, importers, and investors, the category is consolidating fast, and positioning now will set the next decade of margin. With the market heading from USD 574 Million toward USD 1,016 Million by 2030 at 10% CAGR, volume is rising, but excise duties and a Sula-led structure define the terrain.

- For domestic producers: secure estate land in Nashik and Karnataka now, as 85% of output concentrates in two states.

- For importers: target the urban premium niche, where imported wine already holds about 33% share.

- For investors: back challengers like Grover Zampa, where USD 10.4 Million of fresh capital signals consolidation upside.

- For policymakers: rationalize excise, since high duties cap a market growing at 10% CAGR.

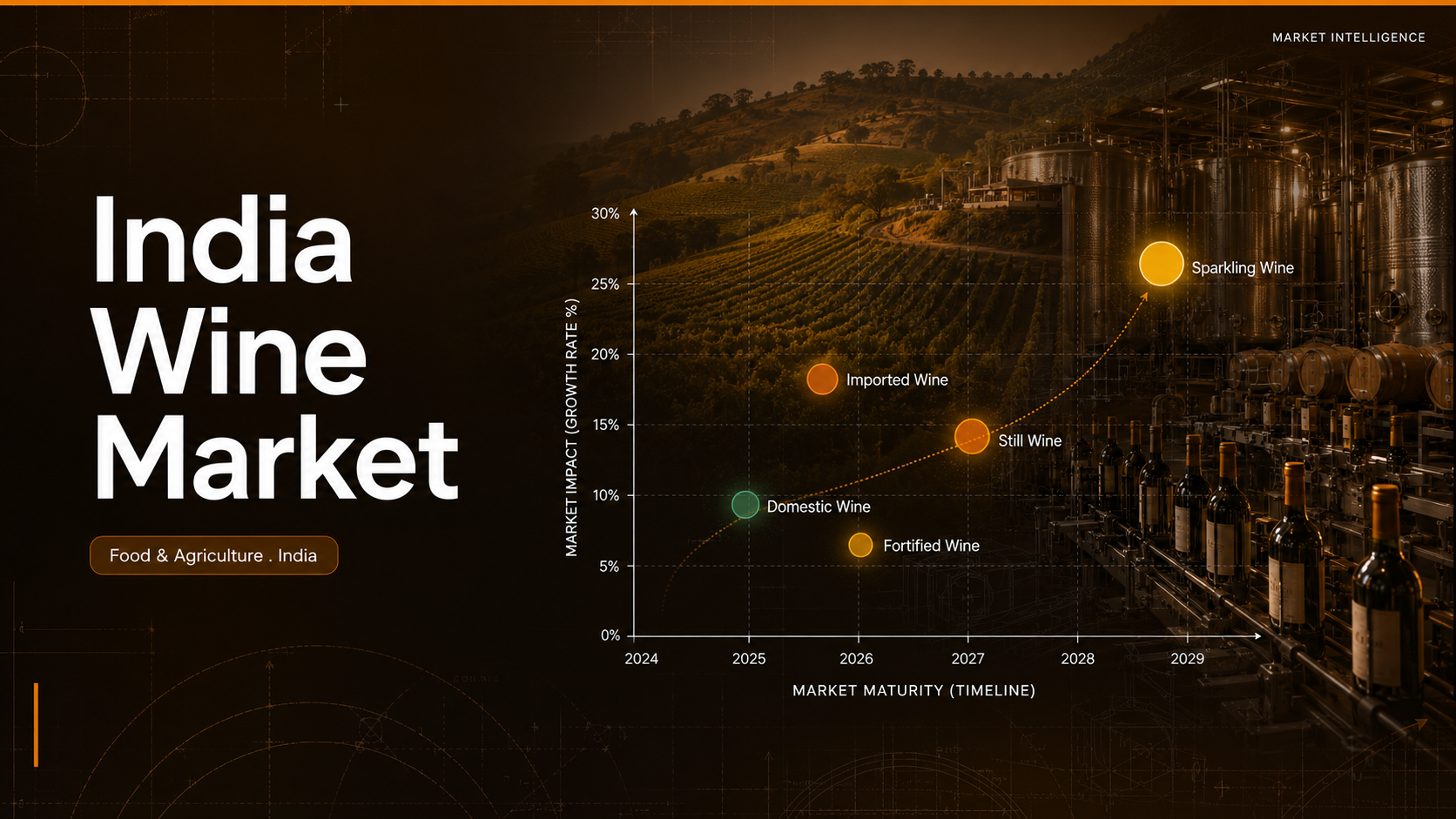

Which Segments and Channels Lead the India Wine Market?

Segment economics favor still wine and the off-trade channel. Still wine dominates volume while sparkling grows fastest off a small base, and red wine leads by color on health-led demand. Off-trade outlets, supermarkets, specialty stores, and online platforms now carry the majority of sales, shifting volume away from the traditional hotel and restaurant on-trade as urban retail deepens. Premiumization is steadily lifting average selling prices across both still and sparkling formats.

- Product mix: still wine holds the dominant share, while sparkling is the fastest-rising format among urban buyers.

- Channel split: off-trade leads distribution as modern retail and e-commerce widen access well beyond the metros.

- Price tiers: domestic labels anchor the mass-premium band, while imports concentrate above INR 1,000 per bottle.

Ken Research Strategic Outlook

The defining tension in Indian wine is not demand, it is taxation and scale. With Sula commanding close to 60% share, the next phase will reward challengers that pair estate capacity with tourism-led brand pull, while excise reform in Maharashtra and Karnataka decides how fast the category reaches USD 1,016 Million. Expect imported labels to keep gaining in metros even as domestic capacity expands near 30%. The next three years will separate scaled estates from boutique labels.

Data Source and Full Analysis

For deeper segment-level analysis, access the full Ken Research report here: India Wine Market Report

Comments

Post a Comment